Strengthening The REIT Regime In Singapore

- MAS measures to strengthen the REITs framework were much awaited though slightly watered down post industry feedback.

- The long-term impact of the proposals will broadly be beneficial to listed REITs while large REIT sponsors and managers such as CapitaLand, Mapletree and ARA may need to factor in additional overheads to ensure compliance.

- We maintain MARKET WEIGHT on REITs with CCT, CDREIT, Starhill and Sabana REIT as our top picks.

WHAT’S NEW

- The Monetary Authority of Singapore (MAS) has refined its proposals to strengthen the REITs market, in response to industry feedback on its consultation paper of 9 Oct 14.

- The amendments to the CIS Code, proposed Notice and Guidelines will take effect on 1 Jan 16, while the proposed amendments to the Act would take effect on 1 Jan 17.

Key proposals include:

Strengthening of corporate governance.

- Related party transactions can be substantial and frequent in REITs, hence managers should be held to a high corporate governance standard. As such:

- Managers and their directors will be bound by a statutory duty to prioritise the interests of REIT unitholders over the interests of the managers and their shareholders, in the event of a conflict of interest.

- At least half of the manager’s board of directors must be independent directors if unitholders do not have the right to appoint the manager’s directors.

- Managers will be required to disclose their remuneration policy and procedures in the REITs’ Annual Reports. This will:

- improve market discipline and the managers’ accountability to the unitholders when setting the remuneration for their directors and executive officers, and

- help investors better understand how potential misalignment of interest has been addressed.

Increase transparency of fee structure.

- MAS will not intervene on the structure of fees or type of fees that managers charge, but will require them to disclose the justification for each type of fees charged. Managers will also have to explain the methodology for computing performance fees, and justify how this methodology takes into account unitholders’ long-term interests.

- This revised position will provide greater clarity to investors on the various types of fees charged by managers, without being overprescriptive on how fees should be charged.

Allow greater operational flexibility.

- The development limit of a REIT will be increased from 10% to 25% of its deposited property.

- In addition, the leverage limit imposed on a REIT will be increased from 35% to 45% of the REIT’s total assets, but a REIT will no longer be allowed to leverage up to 60% with a credit rating.

- These proposed changes will provide a REIT with greater operational flexibility to rejuvenate its maturing portfolio of assets.

- MAS will also continue to allow stapled securities structures with a REIT component to operate without group operational limits. The REIT component will continue to be subject to existing limits.

- MAS noted respondents’ feedback that the existing approaches of relying on:

- unitholders to initiate a review of a manager’s appointment, and

- disclosure to impose market discipline on the use of income support arrangements,

- MAS clarified that, internally managed REIT structures are allowed in Singapore.

ACTION

- The measures were much awaited though a bit watered down post industry feedback. The long-term impact of the proposals will broadly be beneficial for listed REITs while Large REIT sponsors and managers such as CapitaLand, Mapletree and ARA may need to factor in additional overheads to ensure compliance.

- We maintain MARKET WEIGHT on REITs with CCT, CDREIT, Starhill and Sabana REIT as our top picks.

ESSENTIALS

- Much awaited move, though slightly watered down post industry feedback. REITs have been among the top success stories on the Singapore exchange. The proposed changes will strengthen REITs framework improving the long term prospects of the REIT industry.

- Most of the changes were anticipated though some watered down to accommodate views of the industry participants. This includes fee structure changes, key executives remuneration information, income support arrangements etc.

- Large REIT sponsors and managers such as CapitaLand, Mapletree and ARA may need to factor in additional overheads to ensure compliance.

- Measures to strengthen corporate governance will improve the independence of directors and executives of REIT managers, and de-link remuneration to the performance of sponsors and owners of REIT managers while closely tying KPIs to the performance of REITs.

- We believe that these measures will allow REIT managers to remain independent while still being fully owned by sponsors, allowing REITs to continue to tap into sponsorasset pipelines.

- Higher gearing limits of 45% before REITs are required to seek a credit rating could allow the more conservative REITs, where gearing typically does not breach 45%, to save on rating agency fees while the requirement for a rating for higher gearing would curb REITs from taking on excessive debt. Average gearing for REITs under coverage stands at 34%.

- REITs will welcome the larger development limit of 25% (from 10%) of total assets, but it may add to the perceived risk as their incoming producing portion comes down.

- While placing holding restrictions will alleviate the risk, we believe that it may be more appropriate to impose the condition to hold the asset until the full payback period for the CAPEX incurred.

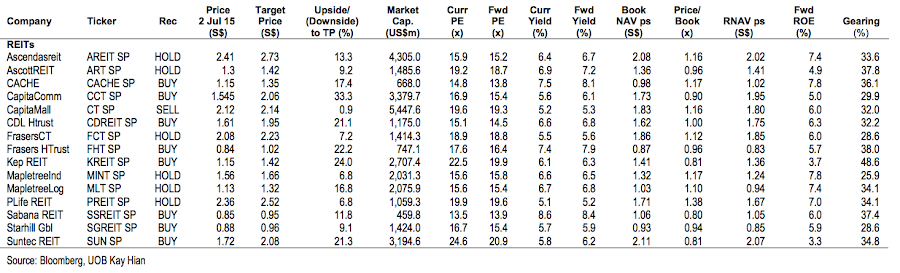

PEER COMPARISON

(Vikrant Pandey, Derek Chang)

Source: http://research.uobkayhian.com/