Hopes pinned on NIM

- NIM trends in focus for 2Q15; loan growth slowing

- Banks should continue to do well; but risk of correction is high as they are a crowded trade

- OCBC remains our preferred pick

Banks have done well, and will continue to do well.

- Singapore banks have been the best performers, rising by 11% over the past 12 months vs ASEAN banks and other Singapore stocks.

- We believe earnings momentum will still be positive with NIM as the key earnings driver despite a much slower loan growth momentum.

- NIM movements are more sensitive to earnings; every 10bps rise in NIM will add 5-7% to earnings, while every 1ppt increase in loan growth would only move earnings by less than 1%.

- Meanwhile, we expect asset quality indicators to remain benign with credit costs staying largely low except for UOB which continues to guide for a 32bps credit cost, higher than peers.

NIM in focus in 2Q15, the key driver to earnings.

- All eyes will be on NIM trends in the upcoming 2Q15 results as banks have stated that the full impact of re-pricing of the SIBOR/SOR hikes would be more visible in 2Q15 in addition to surplus funds (from winding down of trade loans) which were deployed into lower yielding assets in 1Q15, which should have partially reversed.

- NIM should trend up a little for OCBC in 2Q15.

- UOB saw a significant uplift in NIM in 1Q15 and the increase in 2Q15 may not be as significant.

Slower loans; slower GDP ahead.

- Loan growth has clearly slowed and banks are only guiding for mid-single digit loan growth for 2015 in the absence of currency effects.

- Mortgages seem to be ploughing on fairly strongly at 5% y-o-y based on May-15 stats, with consumer loans growing a tad faster than business loans over the same period.

- Total DBU and ACU loan growth in May stood at only 3.5% y-o-y, the slowest since Mar-10.

- Furthermore, our economist downgraded Singapore’s 2015 GDP to 2.4%, the slowest in six years.

- The slower GDP trend is already reflected in loan growth which has moderated. But we believe NIM is the key offsetting factor but this would hinge highly on expectations of eventual Fed rate hikes and sustained high SIBOR/ SOR trends.

Crowded trade; risks are there.

- Although momentum is positive for banks, the sector is a crowded trade only by virtue of the lack of catalysts in other sectors within Singapore and among ASEAN banks. Singapore banks are a safer haven as there is no capital raising risk and asset quality issues.

- But a slight disappointment in earnings momentum and a significant market correction would pose a sell-down risk to the Singapore banks.

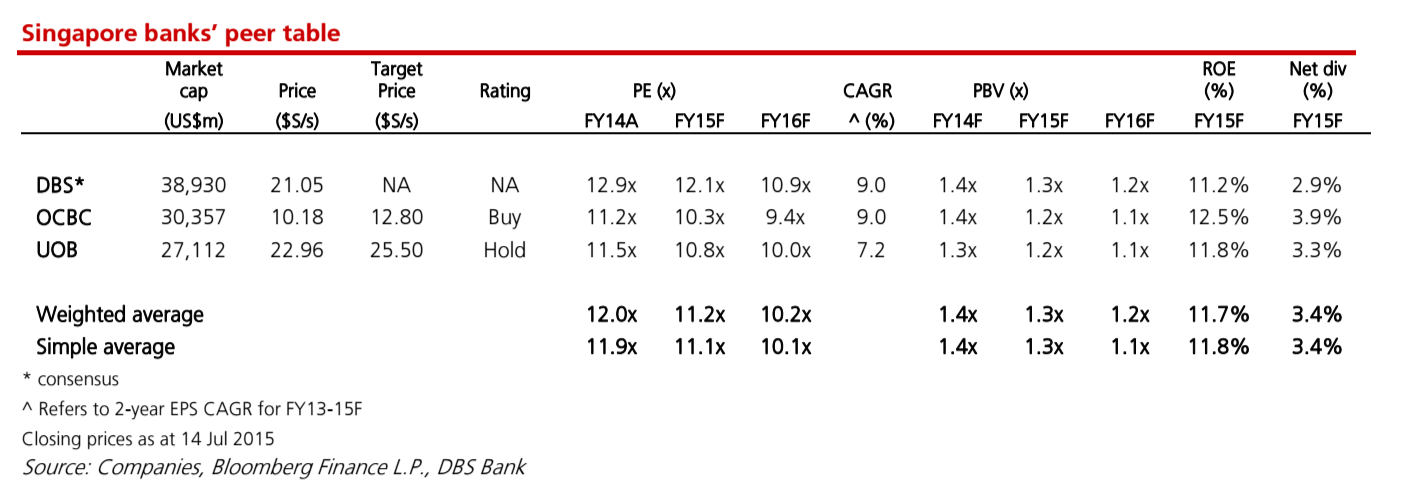

OCBC remains our preferred pick.

- We remain convicted on our preference for OCBC (vs UOB) as we believe market is still under-appreciating its Greater China presence as well as its fee income franchise and low credit cost position.

Riding on its unappreciated Greater China franchise.

- We believe the market is still under-appreciating the OCBC-WHB’s franchise in Greater China.

- With its enlarged Greater China presence, OCBC’s growth prospects in wealth management, retail & commercial banking and insurance are further enhanced.

- Active cross-selling for OCBC’s private banking and insurance businesses are key wins.

- Integration is still on-going but signs of improvement are visible in its wealth management income line.

Solid non-interest income franchise to drive earnings.

- We expect wealth management income to continue its upward trajectory, potentially contributing up to 20% of non- interest income (excluding insurance).

- Insurance contribution could be volatile due to interest rate movements. As such, underlying growth in new business embedded value and total weighted sales should be the focus parameters for insurance, and these have been robust.

UOB remains a HOLD as we believe its missing links are not in the price.

- UOB has been known for its conservative growth but we believe the market may have overlooked the lack of its fee income differentiation as well as Greater China presence.

- We believe over time, regionalisation beyond ASEAN would need to improve to prompt a re-rating for the bank.

- In addition, a stronger traction in non-interest income away from loan- related activities could add a re-rating sentiment. UOB is more Singapore-centric compared to peers with 53% and 44% of its loans and deposits being S$-based respectively.

- While this is not necessarily a weakness, it would remain a point of contention when peers are able to reap better contribution from overseas operations.

- These factors justify our HOLD rating.

(LIM Sue Lin)

Source: http://www.dbsvickers.com/