- We see the recent MAS enhancements to the REITs regime as more tinkering the edges, rather than earth-shattering.

- MAS did not proceed with its most unpopular proposals, particularly those pertaining to performance fees and acquisition/divestment fees, which REIT managers had previously deemed "over-prescriptive".

- At such, we do not expect a major re-rating catalyst for the overall sector.

- The market’s immediate reaction to this is likely neutral or mildly positive.

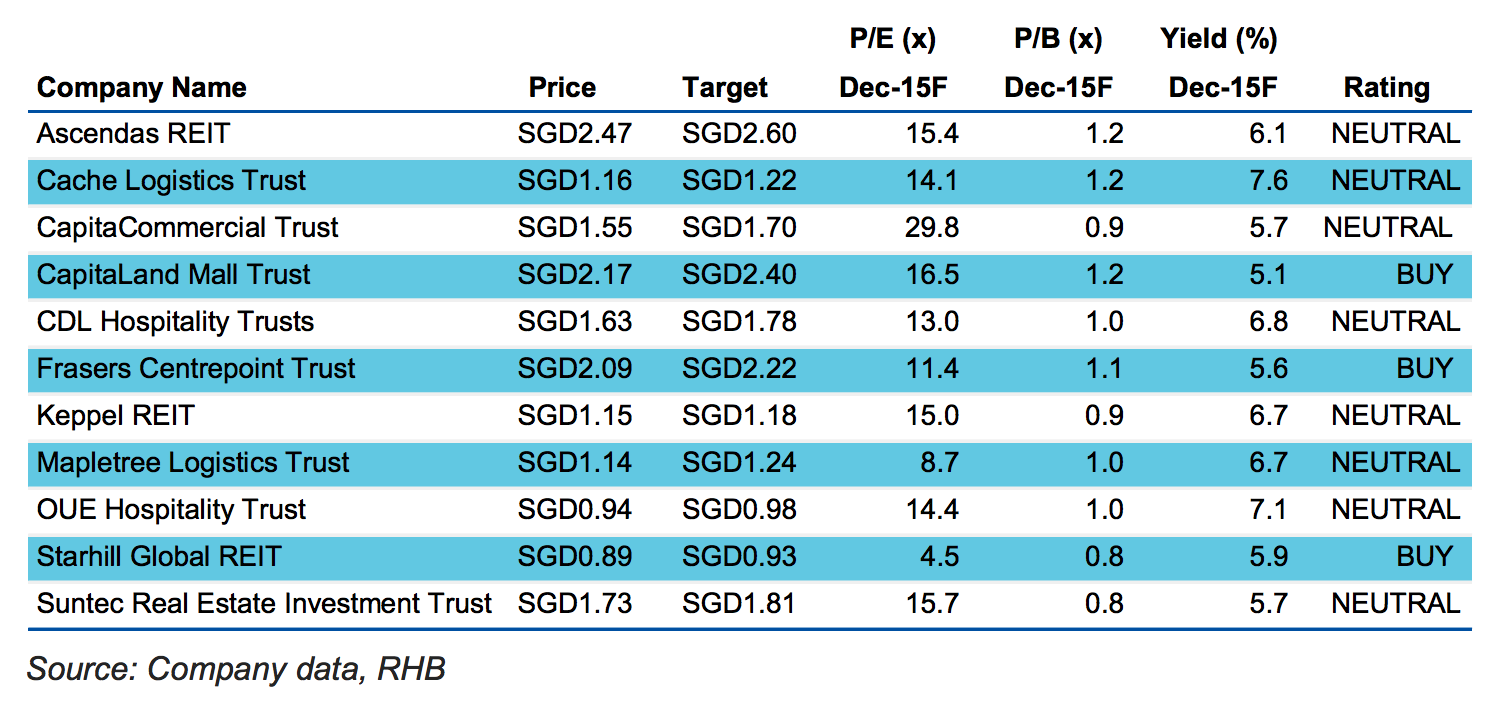

- Reiterate NEUTRAL, with sole preference for retail REITs.

- Top Picks are Frasers Centrepoint Trust, Starhill Global REIT and CapitaLand Mall Trust.

Statutory duty to prioritise the interests of REIT unitholders.

- In terms of degree, we view the Monetary Authority of Singapore’s (MAS) decision to impose a statutory duty on the REIT manager and its individual directors as being the most severe.

- We think this will help to safeguard unitholders’ interests in interested/related-party transactions moving forward. For example, the onus will be on the REIT manager to justify DPU yield accretion in future “sponsor” injections.

- Likewise, income support arrangements for any new acquisitions will probably be tightly-scrutinised to ascertain that the REIT manager does not prioritise the “sponsor’s” interests over that of unitholders.

Single-tier leverage limit of 45% for S-REITs.

- We think Singaporelisted REITs (S-REITs) that are geared near the 45% limit may face near-term pressures to reduce their leverage. Equity fund-raising (EFR) may thus be an option to deleverage.

- We identify three S-REITs that have debt levels near the threshold, namely Keppel REIT (KREIT SP, NEUTRAL, TP: SGD1.18), OUE Commercial Trust (OUECT SP, NR) and Viva Industrial Trust (VIT SP, NR).

25% development limit for existing property.

- We think S-REITs that are holding older-yielding assets stand to benefit from the extra allowance to rejuvenate their properties.

- A lingering concern, however, stems from MAS’ stance to lower the maximum leverage for REITs to 45% from 60% (with a credit rating) and at the same time provide for an additional allowance of 15% for redevelopment.

- This will likely cause some REITs to have to go to the equity markets to raise funds to finance the redevelopment projects, if they cannot fully debt-fund the redevelopment (exceeding the 45% mark) or come too close to the threshold, which may de-rate their share prices.

Peer Comparison

(Ong Kian Lin, Ivan Looi)

Source: http://www.rhbgroup.com/

Source: http://www.rhbgroup.com/